.webp)

Same story, different day/week/month. Energy observers are living Groundhog Day as the US/Iran conflict is entering its 4th month. Oil market fundamentals are tightening daily, although ongoing US/Iran peace discussions and the AI boom have lulled markets into what is potentially dangerous complacency. Until the dust settles around Iran, it is becoming increasingly apparent that investors have a hands-off approach regarding the energy sector. Incorrect in our view, but it’s hard to argue against this “apathy until clarity” approach when energy’s weighting in the S&P500 is a pittance (~3.3%). However, the investment case for both oil and energy stocks is improving and the opportunity to make money will eventually pull attention and capital back to the sector.

Following last month’s all-Iran commentary, this month we’ve returned to our typical format of discussing a broader range of energy topics.

Energy Macro

The US/Iran conflict is now in Week 12, while the ceasefire is now in Week 7. A peace deal has been rumored almost continuously. The most recent iteration involves a re-opening of the Strait of Hormuz, while nuclear negotiations are pushed out a few months. Eventually, a peace rumor will become a peace fact and Charlie Brown will be able to kick Lucy’s football. Of course, the texture of any go-forward normalcy will matter significantly.

Meanwhile, the global supply chain has scrambled effectively to keep markets supplied. Previously stranded oil (sanctioned Russian and Iranian barrels) has moved to consumers. Strategic reserves are being utilized – the US recently saw the biggest SPR drawdowns in its history, while China has halted high-priced imports and is presumably drawing down on its internal inventories (acquired at much cheaper levels). Oil is moving to the markets with the highest spot prices – resulting in record level of US exports. So far, the globe has had enough physical buffers and political jawboning to avoid sustained demand-killing price levels, but storage tanks are not endless.

We are watching Strait of Hormuz tanker traffic and global inventories as our guideposts for the post-war outlook. These continue to signal a tight and tightening market – which is reflected in 2027 NYMEX futures that are now ~$73/bbl compared to low $60s/bbl pre-conflict. We stick with our view that WTI is likely to average $75-$85/bbl for the next few years, with upward bias if the conflict drags through the summer and into Fall, which is very possible. Markets have yet to make this jump – whether due to distraction (AI boom!) or disbelief (speed of conflict resolution, oil demand will decrease, oil supply will increase). We are in Show-Me mode around oil flows, while the market is in Show-Me mode around the sustainability of tightness. Time will tell.

Oil Market Tidbits

Observations:

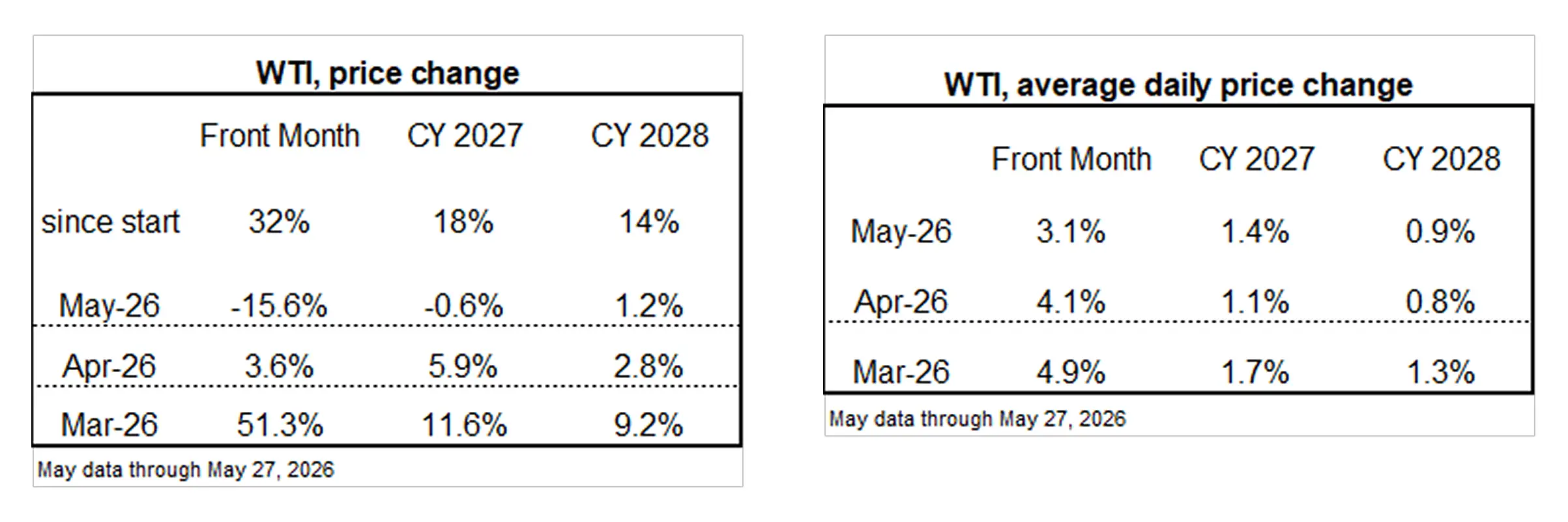

- Near term prices have risen more than longer-term prices – to us, this makes sense given the likelihood that Iran-driven supply challenges will be ameliorated over time.

- WTI volatility, defined as the average daily price change, has declined each month since the conflict started. Markets are getting numb, bored, and less interested. Understandable, but probably unsustainable (and potentially dangerously complacent).

- Despite a feeling that markets are ignoring the reality of increasing tightness, price has consistently inched upward.

- Calendar 2027 futures have moved from ~$62.10/bbl to ~$69.30/bbl (end March) to ~$73.40/bbl (end April) to ~$72.95/bbl (May 27th)…an increase of +18% since the start of the conflict

- Calendar 2029 futures have moved from ~$61.40/bbl to ~$67.05/bbl (end March) to ~$68.95/bbl (end April) to ~$69.80/bbl (May 27th)…an increase of +14% since the start of the conflict

- Remember the quote used frequently by Mark Twain: “There are three kinds of lies: lies, damned lies, and statistics.”

Energy Industry Behavior

Capital discipline remains the overall mantra of the energy industry. Higher cash flows driven by higher commodity prices are mostly being directed toward debt paydown, share repurchase and higher cash balances. We expect this to broadly remain the case until 1) there is less volatility/noise in the front portion of the oil curve, 2) forward oil prices move sustainably into the mid $70’s and 3) investors begin to favor growth.

That does not mean, however, that there are not signs of longer-term optimism and offense on display in the oilpatch. There are plenty of moves being made that signal confidence in a favorable outlook:

- Rigcount has ticked up slightly. The week before the conflict, the Baker Hughes oil rigcount was 407. It remained flattish for March and April, but increased to 425 during May (an increase of +4% from pre-conflict levels).

- Selective upstream capital spending increases. We believe the macro writing is on the wall that will incentivize higher levels of oil-weighted upstream spending. Nonetheless, the industry is likely to babystep its way to higher activity levels. Overall, the 2026 capital spending forecast for PEP Research’s upstream coverage has moved up a mere +1.1% since the start of the year. However, almost half of the covered oil-focused companies (7 of 13) have seen an uptick in spending expectations (outright capex increases or movement to the higher end of previously guided ranges). Of note was Diamondback Energy, which indicated a “green light” investment scenario had emerged, improving from the prior “yellow light” environment.

- Healthy market for assets. Even before the Iran conflict and the runup in oil price, US shale assets were enjoying robust values as established and new companies were jockeying to add inventory/runway in a maturing US market. In a marked contrast to the 2025 Liberation Day tariff reaction, currently neither buyers nor sellers have walked away from oilpatch asset deals due to volatility/uncertainty. Values have drifted (but not exploded) higher, but we have seen neither excess greed nor excess fear.

- Boomer of a New Mexico lease sale. For quality assets, you buy when you can, regardless of macro conditions. Multiple companies paid gargantuan lease bonuses in last week’s New Mexico lease sale. Devon was the highest profile bidder, spending over $150k per acre (and ~$2.6B in total) for core Permian acreage.

Corporate consolidation returned during May. As AI/data center projects get bigger, the companies providing the power are also getting bigger. NextEra Energy announced a deal to acquire Dominion Energy – creating the world’s largest electric utility. Together, these two players have an enterprise value of almost $400B, with NextEra trading at almost 22x 2026 earnings projections. Power isn’t sleepy anymore! In traditional oil and gas, Shell sized up in Canada’s Montney shale, paying ~$14B via a 25%+ premium to acquire ARC Resources. This was the first public-to-public upstream deal since Devon/Coterra was announced in early February. Our expectations have been for a generally slower corporate M&A market until Iran settles down. But perhaps the Shell-ARC combination indicates the big boys will look past the macro noise to do deals…maybe frontrunning higher values that will likely emerge with resolution of the Middle East situation.

Energy Stocks

As shown in the table below, energy stocks have been great performers YTD, meaningfully outpacing the broad market. But in multiple ways, it is really a story of Before and After. Energy stocks ripped before the Iran conflict started, outperforming when the tech sector was struggling. Counterintuitively, energy has lagged the broader market after the beginning of the war. We must look deeper to get a better picture. Before the cease fire was announced on April 7th, energy stocks were up on an absolute basis and outperforming a declining stock market. After the cease fire was announced? The market took off (fueled by tech/AI), while energy has declined/lagged.

The master-of-the-obvious takeaway here? A Middle East conflict is bad for the market and good for oil/energy stocks. Being on the path to a resolution of a Middle East conflict is good for the market and bad for oil/energy stocks.

Buried in these numbers is the reality that the cease fire in Iran, while trending toward peace, did very little to change the oil market fundamentals. Oil didn’t start flowing. Inventories kept drawing. The cease fire showed we were on a path toward good things happening. But the longer the path, the tighter the market will be when a resolution is actually achieved. This is the leap that a tech-obsessed market has not yet made.

We get it. It’s hard to pay attention to a sector that’s only 3.3% of the S&P500, driven by a falling commodity price and a (seemingly) resolving geopolitical crisis. Particularly when 30%+ of the S&P500 is going nuts to the upside with trillion-dollar market cap companies gaining 5% daily.

Hence, for energy, it is apathy until clarity.

- Clarity might come in the form of a tech pullback that leaves investors with a willingness to evaluate other sectors and cash they are looking to redeploy, OR

- Clarity might come in the form of a resolution of the Middle East conflict and a non-war-influenced oil price. That likely $75-$85/bbl WTI oil price (our base case) and the associated energy company profitability will be harder to ignore, OR

- Clarity might come in the form of a rekindling of military activity and the realization we are not on a path toward resolution, OR

- Clarity might come in the form of a non-resolved conflict/ongoing ceasefire for so long that supply cushions are exhausted, oil inventories are pushed to operational minimums, and prices move to a demand-destroying level that can’t be ignored, OR

- Clarity might come in the form of us being flat-out wrong and the sector gets hit over the head with supply/demand imbalances (or some other situation) that make oil prices and current stock valuations unattractive

We think the deck is stacked in favor of patient energy investors. As stated recently, we see every dip as an opportunity to add to energy positions. It isn’t sexy, it isn’t outperforming right now, but it is going to be rewarding when clarity arrives.

As always, we welcome your questions and comments.

(1) Bloomberg